|

|||

|

|

|

||

|---|---|---|

|

||

|

||

|

||

|

||

|

|

|

|

Should You Refinance Your Home: Key Considerations and What to ExpectRefinancing your home can be a strategic move to save money, reduce monthly payments, or tap into your home's equity. However, it is crucial to weigh the benefits against the costs and understand the process before making a decision. Understanding the Basics of Home RefinancingRefinancing involves replacing your existing mortgage with a new one, often to secure a lower interest rate or change loan terms. It can also be a way to access cash by borrowing against home equity. Benefits of Refinancing

Costs Involved in RefinancingWhile refinancing can offer savings, it's essential to consider the associated costs, such as application fees, appraisal fees, and closing costs. These can sometimes offset the benefits of refinancing. When Is the Right Time to Refinance?The timing of refinancing can greatly impact its effectiveness. Here are some situations where refinancing might be beneficial:

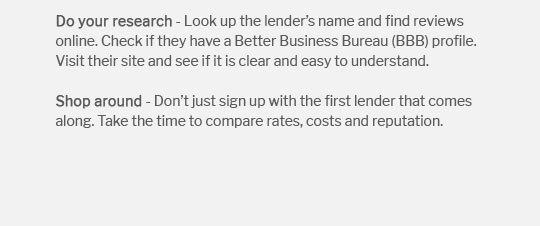

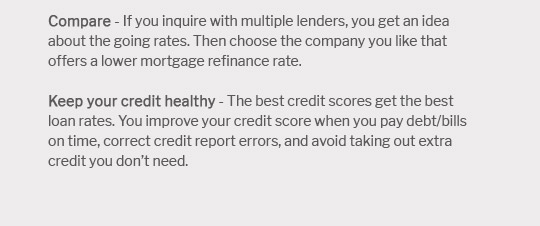

Steps to Refinance Your HomeEvaluate Your Financial SituationBefore refinancing, assess your financial health. Determine your home equity, credit score, and debt-to-income ratio to understand your refinancing eligibility. Shop for LendersCompare different lenders to find competitive rates and terms. Consider using online tools to explore offers, such as a refinance fixed home loan calculator for personalized estimates. Prepare DocumentationGather necessary documents, including income statements, credit reports, and tax returns, to streamline the application process. FAQs About Refinancing Your Home

In conclusion, refinancing your home can offer significant financial benefits, but it's essential to carefully consider the timing, costs, and potential savings. By evaluating your financial situation and exploring options, you can make an informed decision that aligns with your long-term financial goals. https://www.ramseysolutions.com/real-estate/is-a-mortgage-refinance-right-for-you?srsltid=AfmBOoqkU_ri02LB3vOSyxSR7vR7tJMLAlAuwkO6qf00bv8R0UiVlJTo

Refinancing your mortgage is usually worth it if you're planning to stay in your home for a long time. That's when a shorter loan term and lower interest rates ... https://www.citizensbank.com/learning/refinancing-your-mortgage.aspx

Refinancing could lower your interest rate, change your loan type, adjust your repayment term, or cash out available equity. Visit Citizens to learn about ... https://yourhome.fanniemae.com/own/mortgage-refinance

Refinancing may be able to lower your monthly payments, shorten the term of your loan, or offer a bit more financial security.

|

|---|